Business Foreclosure: What to Do

The term “business foreclosure” is usually associated with the foreclosure of business property, but it can also refer to the legal process of shutting down a business. If your business is facing foreclosure, it’s important to understand the process and your options.

When a company goes bankrupt, many owners are frightened and unsure of what to do. The good news is that you may take precautions to safeguard your business and limit harm.

Business foreclosure, a term traditionally linked with the repossession of property due to unpaid loans, also refers to the broader scenario of business dissolution due to financial distress. This distress often comes from from financial mismanagement, unrealistic business plans, insufficient capital, and the broader economic environment, leading to a struggle to maintain loan payments. The process changes by state, offering either a judicial route involving court procedures or a non-judicial path that allows for quicker property repossession and sale without court intervention.

Solutions to avoid foreclosure include negotiating payment suspensions or loan modifications with lenders, refinancing, seeking investments, or leveraging personal loans. For those already in the foreclosure process, options such as filing for bankruptcy, surrendering property, or selling the commercial property to satisfy debts are possible. Recovery post-foreclosure involves rebuilding credit, budgeting, and dealing with the waiting periods before reentering the borrowing market, showing the importance of financial prudence and exploring all possible avenues to getting away from foreclosure.

This blog post will prepare you for business foreclosure by discussing many important topics, explaining some key terminology, and listing options.

Table of Contents

What is a Business Property Foreclosure?

Foreclosure is a legal process that allows creditors to collect unpaid debts by selling or seizing the property used as collateral for the loan. When a business owner fails to make payments on their business loan, the lender may initiate foreclosure proceedings.

The lender takes possession of the property or assets specified in the lending agreement. This is generally the case with company premises. The lender will start a foreclosure procedure when a borrower cannot make payments from collateralized loans.

What Causes Foreclosures of Businesses?

The most common reason for company foreclosures is the mismanagement of funds. New business owners frequently underestimate expenses and overestimate their prospects. Running a business is difficult, and most businesses fail in their first five years of operation.

The main reasons for foreclosure of a business are:

- mismanagement of funds;

- unrealistic business plan;

- insufficient capital;

- poor management;

- business location;

- economic slowdown or recession.

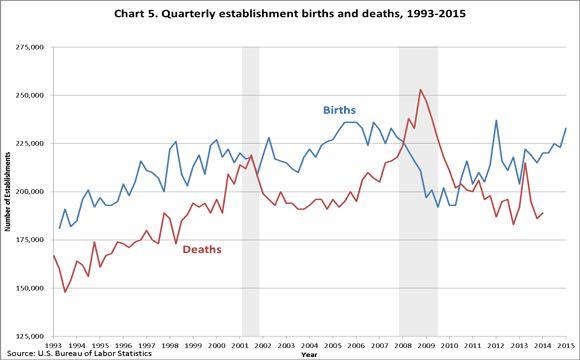

For example, in the 2008 recession, many business owners could not keep up with their mortgage payments and subsequently lost their businesses. It’s estimated that between December 2008 and December 2010, as many as 1.8 million small businesses had to close.

This U.S. Bureau of Labor Statistics chart shows how during recessions, there are fewer new businesses open and more closed. This trend tends to recover shortly after the recession.

Rates of Business Foreclosure Across the States

According to recent statistics, business foreclosure rates are highest in the following states:

- Nevada

- Arizona

- California

- Idaho

- Utah

These states have been hit hardest by the recession, and business owners in these states are more likely to default on their loans. If you live in one of these states, it’s important to be extra careful about managing your finances and making sure you can make your loan payments.

In Florida, business foreclosure rates have been increasing in recent years. This is due to a large number of small businesses in the state and the fact that many business owners took out loans during the housing boom and are now struggling to make their payments.

How Many Types of Business Foreclosures Are There?

Some lenders can use a streamlined non-judicial foreclosure procedure in certain states, while others must follow the state court system – a judicial foreclosure. This blog post can learn all about commercial real estate foreclosure types.

Judicial Foreclosure

A borrower’s right to refinance begins when the lender files a claim or petition with a court. If the lender obtains a foreclosure judgment, the property is sold to pay off the outstanding mortgage debt. Because the lender is not required to use a foreclosure sale, it has no choice but to sue the borrower to get an outcome. Because this process might take months or even years, lenders prefer it as a last resort. For the borrower, this allows them to work through a solution.

Judicial foreclosure is the norm in 22 states, including Florida, Illinois, and New York.

Non-judicial Foreclosure

Non-judicial foreclosure occurs when a loan agreement includes a power of sale clause. The main advantages are:

- The least amount of processing is required;

- The lender does not need the courts to take action against the borrower.

Before selling a property at auction, the lender must follow statutory procedures. After executing the necessary procedures, the lender may sell the property at a foreclosure sale.

The remaining 28 states, including Arizona, California, Georgia, and Texas, primarily utilize non-judicial foreclosure, often known as the power of sale.

Are There Alternatives to Business Property Foreclosures?

It is feasible to contact the lender and request a suspension of payments for a short time. If the company owner can show the lender that future payments will be made, this option may be acceptable to the lender.

Most small- and medium-sized company owners will be asked to provide a personal guarantee when their property is registered in their business name. If the company owners cannot pay the loan back, they risk losing their assets collateralized. Borrowers could demand it as an alternative if this did not happen.

Consider bringing in an investors

If your company concept is sound, venture capitalists might be interested in investing. Because they are concerned about the problem, they may be willing to take a greater percentage equity stake. When venture capital firms are unwilling to step in, angel investors may be ready to help.

Consider refinancing

When dealing with lenders, inquire whether refinancing is an option. The terms are likely to be less favorable, but at least the company may continue operating.

Consider asking for a loan

Another option is to ask family and friends for a loan so that your payments stay on track. The disadvantage of this choice is that things could get heated if you cannot pay them back. This can lead to conflict between friends and family.

Can Foreclosures Be Prevented?

Foreclosure is not a popular option among loan providers. It may take months to complete, requiring the services of attorneys and courts. Foreclosure prevention may be possible when lenders are ready to arrange with the borrower.

A pre-negotiation letter

Lenders often require a pre-negotiation letter with business property foreclosures. This is a contract concerning the length of the negotiation. The way to transfer a business property is more formal than the method for transferring a household asset. It’s used to avoid confusion during negotiations.

Act before lawyers get involved

It’s critical not to wait when your company is facing foreclosure. Once a foreclosure is initiated, attorneys become involved, and their fees accumulate daily. To reinstate the property, the borrower must pay these costs. These charges may be negotiated down to smaller amounts, but this is not always the case.

Foreclosure documents are sent by the lender, after which borrowers have a specific length of time to pay off their debts in default. If you can pay the debt in full before the period expires, you will be able to avoid foreclosure. The lender may demand additional fines and interest if you do not make the payment on time.

Before seizing property, the lender must follow certain legal procedures. A borrower may have legal options against foreclosure if the lender does not follow the appropriate methods. However, in the rare event that one of these things occurs, they are most likely considered a Hail Mary pass for the borrower.

Five Alternative Options

Alternative financing choices, loan modifications, commercial property surrender, and bankruptcy are just a few of the numerous options for avoiding foreclosure.

#1: Look For Alternative Financing Options

There may be other loan options to assist you in keeping your company afloat. Use your accounting software to examine your financial records and see whether they owe you money. If your receivables increase, ask those who owe you money for payment.

Merchant cash advances (MCAs) are another choice for short-term liquidity. The idea is to sell a percentage of your future credit and debit card purchases. The cash is typically accessible in a few days when you use invoice factoring or MCAs.

#2: Request Loan Modifications

Borrowers who have trouble making payments should contact their lenders as soon as possible. They can use loan modifications to help them make ends meet. The interest rate or the loan term may be decreased or extended by the borrowers.

It’s also conceivable that the loan will be repaid in full. Lenders may also be ready to reduce the principal on outstanding loans.

Lenders are more likely to accept loan modifications due to the foreclosure procedure. It can take weeks, if not months, to resolve a case. The bank will probably lose money in this situation.

#3: Consider Protection from Bankruptcy

Filing for bankruptcy can assist small businesses in avoiding foreclosure. The borrower might be able to keep possession of the property.

- Chapter 7 bankruptcy is about forgiveness and offering assistance to debtors, regardless of the number of obligations owed or if the person is solvent or insolvent. In the United States, a few portions of bankruptcy legislation might be beneficial. As a consequence of the ruling, other business assets might be taken. The property, however, may be seized by the lender.

- Business owners may keep the property even if they file for Chapter 11 bankruptcy.

- Chapter 13 might be utilized to pay down some of the debt while the rest is released regarding debt elimination.

- The objective of Chapter 12 is to assist farmers and fishermen.

#4: Surrender Commercial Property

A commercial property may be surrendered to relieve the debt burden. A sale is similar to a foreclosure, but it’s usually known as a deed rather than a foreclosure. As opposed to litigation, this process is completed through mutual agreement. For commercial real estate transactions, the split is more popular.

The distinction between the amount owed and the property’s market value is a deficiency judgment. Deficiency judgments are possible under state law.

If the debt amount is much higher than the property’s value, the bank may demand additional conditions to account for this risk.

#5: Sell the Commercial Real Estate

The lender could purchase the property at the foreclosure sale based on the credit. The lender will offer a “credit bid” at the foreclosure sale so that they won’t put any cash up. The lender will not qualify for a deficiency judgment based on the total debt owed by the borrower, including the principal, interest, late fees, attorneys’ fees, and foreclosure costs.

If no third party offers a higher price than the credit request, the lender obtains ownership of the commercial property. If a third party outbids the lender, the property is transferred to that individual. After the sale, the funds are used to pay off the mortgage.

What happens when a bank forecloses on your business?

A: Foreclosure is the legal act of taking back property from a debtor because they have defaulted on payments (failed to keep up with payments or perform other loan conditions). Individual U.S. states have enacted foreclosure laws.

Banks may try to recoup money if borrowers stop making payments by taking legal action against them. They can, for example, take control of your property and sell it to pay off the mortgage on your home. Once more: The business owner pledged real estate and personal assets in many circumstances. Personal assets of the company owner, such as their home or automobile, are examples.

If the borrower does not pay, the lender wants a security interest in the property. If the borrower defaults on the loan, the purchase agreement includes a clause that allows the creditor to reclaim the property. In certain circumstances, an acceleration clause may be included in the agreement, allowing the borrower to be responsible for the whole amount of the defaulted loan.

When the credit is authorized, a copy of the default notification is sent to the debtor, who has a certain amount of time—typically a redemption period—to correct the situation. During this period, the person may seek to make the debt current, negotiate settlements with creditors, or go bankrupt, all dependent on state legislation.

If the borrower cannot cure the default within the time limit, their property may be seized and sold, with the funds going first to the lienholder and others who hold liens on the property. In some states, the lender can place a personal judgment on the debtor for the remainder owed after the sale.

What if the business owner committed personal assets as collateral?

The foreclosure procedure is the same for commercial and residential properties. Commercial property foreclosure would present several challenges if the company owner committed personal assets in addition to the property. This may cover the business owner’s house or automobile.

In most situations, a personal guarantee is given by the business owner to secure payment of the loan. The business owner will be named a guarantor in the foreclosure lawsuit, and the company itself will be sued.

What is the Simplest Solution for Foreclosure?

The fallout of foreclosure affects everyone involved. The majority of lenders are ready to alleviate the negative consequences on the borrower by exploring foreclosure alternatives. If you’re having money problems, it’s usually a good idea to contact your lender. Contact the customer before you start missing payments and see if anything can be done. If you start missing payments, don’t ignore your lender’s communications—you’ll get important notifications informing you where you are in the process and what rights and choices you have left.

What does it mean to foreclose a business?

Businesses go bankrupt all the time. Businesses can also fall behind on their mortgage obligations. A mortgage payment due date, or a violation of the loan’s conditions, is considered a default. A lender may file a foreclosure lawsuit against a borrower to sell the property and recoup the money they invested when they fail to pay back their loan.

The commercial foreclosure procedure is comparable to the residential process, except for the appointment of a third-party receiver. Suppose the lender believes that a borrower is an absentee property owner or is neglecting the company’s needs. In that case, it may petition the court to safeguard the investment by naming a third-party “receiver” to run the firm until its sale.

In the event of default, a mortgage provider will generally include a contract provision allowing you to get tenant payments in return for your agreement—and it makes sense. If a company is closing, the owner may keep the profits rather than hand them over to the lender. By collecting the rent and maintaining the commercial property attractive to purchasers, a receiver can guarantee that vacancies are filled and promptly address maintenance problems.

The lender’s request will be granted if the court approves it, at which point the receiver will take control of the company’s assets until the foreclosure sale. The lender may also demand additional assistance. The receiver may be allowed to sell the home before it is foreclosed upon, for example, if the court allows it.

Can you recover from a foreclosure?

Yes, you can recover from a foreclosure. It requires patience, consistent effort, and financial discipline. Here’s a general overview:

Credit Repair: Foreclosure significantly impacts your credit score. Regularly checking your credit report for errors and making timely payments on all remaining debts can help rebuild your credit.

Saving and Budgeting: Foreclosure often results from financial hardship. Developing a strong savings plan and a realistic budget can help prevent future crises.

Reestablishing Credit: Obtaining a secured credit card or a credit-builder loan, and making payments on time can help reestablish your credit history.

Waiting Period: Most mortgage lenders require a waiting period of 3-7 years after foreclosure before you can apply for a new home loan, depending on the loan type and circumstances.

About The Author

Jesse Shemesh

Disclaimer

Please note that Point Acquisitions is not a tax expert or tax advisor. The information on our blogs and pages is for general informational purposes only and should not be relied upon as legal, tax, or accounting advice. Any information provided does not constitute professional advice or create an attorney-client or any other professional relationship. We recommend that you consult with your tax advisor or seek professional advice before making any decisions based on the information provided on our blogs and pages. Point Acquisitions is not responsible for any actions taken based on the information provided on our blogs and pages.

1031 Exchange Capital Gains Tax Deferral

According to a 2021 report by the National Real Estate Exchange Services (RES), over 240,000 1031 exchange transactions were completed in the United States, totaling $100 billion. This impressive figure underscores the role of 1031 exchanges in the real estate…

Read More

1031 Exchange Benefits

As of Q4 2023, the national vacancy rate for all commercial property types in the United States sat at 9.2%, according to CBRE’s latest insights and research. This represents a slight decrease compared to the previous quarter and suggests a…

Read More

1031 Exchange Legal Considerations: A Must-Read Guide

You’re in the right place if you’re considering a 1031 exchange for your commercial real estate investments. Whether you’re a seasoned investor or just dipping your toes into the market, understanding the legal landscape of 1031 exchanges is key to…

Read More